The Impact of CSRD and ESRS on Maritime Sustainability Reporting

The Impact Of CSRD And ESRS On Maritime Sustainability Reporting

Unpacking the Regulatory Shifts and Their Implications for Maritime Companies and Tugboat Operators

In the wake of the European Union’s ambitious Green Deal, maritime companies, including tugboat operators, are transitioning into a time when sustainability reporting will become the norm. The driving force in this change is the Corporate Sustainability Reporting Directive (CSRD) and the European Sustainability Reporting Standards (ESRS), both of which set out to transform how companies report on their environmental, social, and governance (ESG) metrics. This article delves into the regulations and unpacks how they will impact the maritime sector, helping the industry understand the road ahead.

Why the CSRD and ESRS?

The CSRD mandates that all large companies and listed SMEs in the European Union adhere to common mandatory standards for sustainability reporting. To operationalize these requirements, the ESRS were developed, providing detailed guidelines that ensure uniform and comprehensive disclosure across a range of ESG issues. These standards are designed to make the sustainability reports more comparable and reliable, thereby enhancing transparency in how companies impact the environment and society. Thus, while the CSRD sets the stage for comprehensive sustainability reporting by large companies and listed SMEs across the EU, the ESRS provides the detailed script and guidelines, ensuring each actors’ performance is consistent and can be effectively evaluated.

In short, the CSRD and ESRS have two aims. Firstly, they are designed to enhance clarity for investors and, secondly, for aligning corporate activities with the EU’s Green Deal agenda. This dual-purpose aims to standardize sustainability disclosures, which will enable investors and other stakeholders to make more informed decisions based on the sustainability performance of companies, in turn, further redirecting capital towards sustainable businesses. Not only does this encourage companies to adopt greener and more socially responsible practices, it also contributes to the EU’s objective of achieving a sustainable and inclusive economy.

Which companies need to report under CSRD requirements?

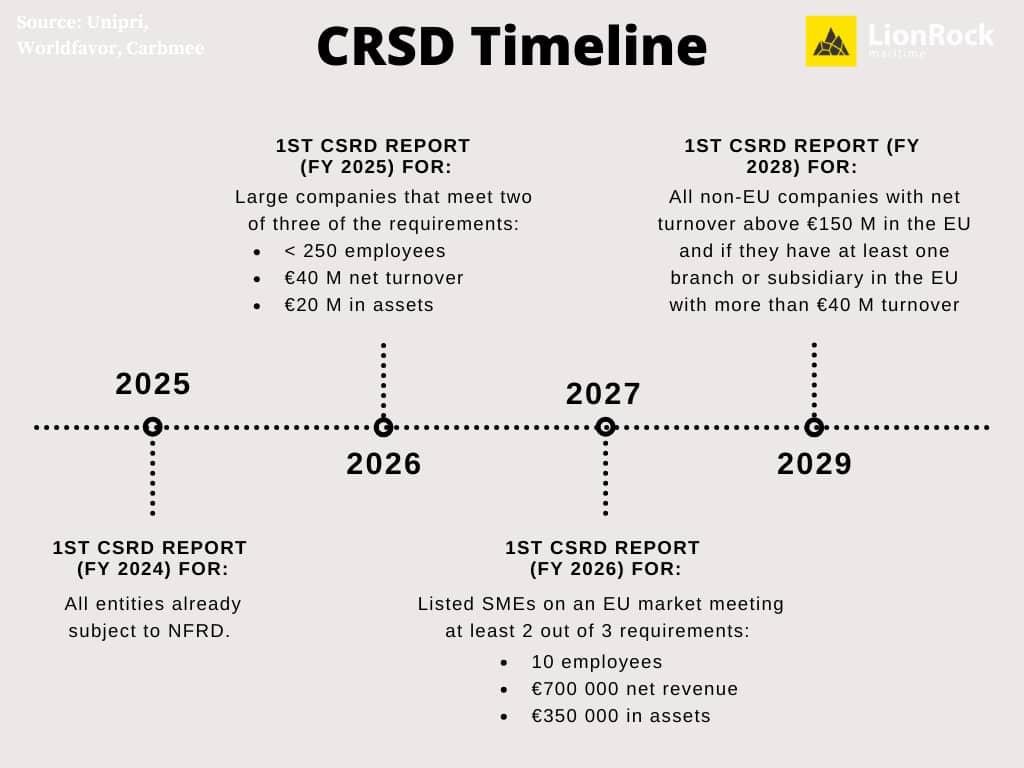

The CSRD will be implemented in phases, starting with companies already subject to the Non-Financial Reporting Directive (NFRD). Gradually, the scope will expand to include all large companies, listed SMEs, and eventually, certain non-EU entities by 2028. This phased approach allows companies time to adapt to the new requirements but also places immediate pressure to start preparing for compliance.

Implementing the ESRS

The ESRS went into effect on January 1, 2024, affecting all companies previously subject to the Non-Financial Reporting Directive (NFRD). Regarding the newly adopted legislation, companies are mandated to report on the following key points:

Companies must report on their emissions, quantitatively and qualitatively. Emission reporting concerns direct emissions (Scope 1), indirect emissions from purchased energy (Scope 2), and other indirect emissions (Scope 3), which include emissions along the value chain, such as those from purchased goods and services, business travel, employee commuting, waste disposal, and use of sold products. For the first reporting year, a company with less than 750 employees may omit scope 3 emissions. In addition to the quantitative metrics on their GHG emissions, companies must provide qualitative information about the data they report. This is to contextualize the data, and provide an overview of the structures in place to manage environmental issues.

The principle of double materiality in the ESRS ensures comprehensive sustainability reporting by addressing financial and impact materiality. Financial materiality focuses on how ESG issues affect a company’s financial performance, influencing investor decisions and economic outcomes. Impact materiality assesses the effects of a company’s operations on society and the environment, considering the significance of the company’s activities on external factors like ecological health. Companies must identify which emissions hold material significance from these perspectives and report them appropriately.

Finally, to ensure compliance and reliability of the reported data, ESRS disclosures are subject to verification. Companies are required to implement robust internal processes to manage data gathering, verification, and reporting, and these processes may also need to be audited by certified professionals. Given the comprehensive nature and novelty of the ESRS, companies might still be adjusting their systems to fully align with these standards. Support and guidelines from the European Financial Reporting Advisory Group (EFRAG), which developed the ESRS, along with assistance from national regulators, is expected to aid companies in this transitional period.

Implications for the Maritime Sector? Sector-specific ESRS

The CSRD and the newly adopted ESRS will change reporting of GHG emissions for the maritime sector. The legislation recognizes that sectors are often exposed to similar sustainability-related risks, just as they often have similar impacts on society and the environment. Therefore, sector-specific standards will also be developed under the ESRS, which will provide the necessary clarity and guidance to address the unique challenges faced by the maritime transportation industry when reporting its emissions. According to Article 29b(1), third subparagraph, of the Accounting Directive sets the adoption date of the sector specific ESRS by mid-2026. The maritime sector must wait for reporting standards that provide clearer guidance, and for now rely on the general guidelines of the CSRD.

While the ESRS sector-specific reporting standards are not yet known, the classification of the sector is. The ESRS define marine transportation as consisting of undertakings that provide deep-sea, coastal, and/or river-way freight shipping services. Key activities include transportation of containerized and bulk freight, including consumer goods and a wide range of commodities. This also includes the transport of passengers or freight over water, whether scheduled or not. Also included are the operation of towing or pushing boats, excursion, cruise or sightseeing boats, ferries, water taxis etc. The section below will elaborate in-depth on how tugboats might are affected.

Impact of CSRD on Tugboat Operators – Materiality and Indirect Emissions

In line with the criteria for large companies and publically listed SMEs listed in the timeline, it is reasonable to conclude that a relatively small portion of tugboat operators meet these criteria, and will thus be directly impacted by the CSRD. Nonetheless, although the CSRD first has to be reported by large and EU-listed companies, the entire value chain of these companies are indirectly impacted. As part of the value chain of larger companies, who are subject to report on the CSRD, tugboats are considered part of their indirect, scope 3, emissions.

The directive states that information about each actor in the value chain is not required unless it pertains to ‘material’ upstream and downstream value chain information. The concept of “materiality” plays a central role here, indicating that emissions from tugboats would need to be included if they are significant in relation to the vessel operator’s environmental impact. In analyzing the materiality of tugboat operators, companies need to consider their environmental and financial impact. First, if greenhouse gases emissions and other pollutants of tugboat operators contribute significantly to the company’s total environmental impact, they are likely to be deemed material. Next, financial risks and opportunities associated with tugboat operations, such as potential costs related to fuel consumption, emissions regulation compliance must be considered, along with the potential for investment in cleaner technologies. Thus, the emissions from tugboat operations could be substantial enough to warrant consideration under the CSRD’s scope of reporting, particularly if the towage operations have, for example, inefficient fuel usage. In the end, it depends on the context of the company and their tugboat operator.

Data transparency is required for the whole value chain, and companies are encouraged to strive for the most accurate data possible. Data from other parties in the value chain need to be sent at the request of firms, as these emissions must be included in their annual sustainability reports under the CSRD. Only in cases where precise data is not available or practical to obtain, are companies allowed to use estimates based on average consumption. This can involve using established industry averages, emissions factors, or other estimation methods that reflect the typical emissions produced by such activities. This is particularly important for emissions sources where the company does not have direct control or complete data visibility, such as those involving third-party services.

It is clear that the scope 3 emissions still leave some uncertainties, specifically regarding the definition of materiality and data transparency. For third-party services such as tugboats and other port operations, answers are likely provided once the sector-specific ESRS guidelines are out by 30 June 2026. While it is possible that the emissions of tugboats can be estimated, it is more likely that they will require accurate measurement, given this is possible. Lastly, a committee has been established to review the act at least every three years, suggesting the framework is evolving. This could lead to more specific guidelines on reporting emissions, as the CSRD is implemented.

Challenges and Opportunities for Tugboat Operators

Precisely calculating emissions from maritime operations, including those from tugboats, presents several significant challenges that can contribute to administrative burdens for companies. Firstly, the variability in tugboat operations – affected by factors such as differing fuel types, operational conditions, and aging fleets – complicates the accurate measurement of emissions. Collecting consistent and reliable data across diverse operational scenarios demands robust tracking systems and potentially significant investments in technology and training.

The administrative load is further increased by the need for ongoing data verification to meet reporting standards under regulations such as the CSRD. This involves not only the initial setup of measurement and reporting systems, but also their continuous management and updates to comply with evolving standards and technologies.

At the same time, the pursuit of precise emissions calculations opens substantial opportunities for the maritime sector. Enhanced accuracy in emissions reporting drives greater transparency, providing clear insights into environmental impacts and operational efficiencies. This visibility can lead to better-informed decisions by stakeholders, including investors, regulators, and customers, who are increasingly valuing sustainability.

The focus on detailed emissions data encourages companies to adopt more sustainable practices. Identifying specific sources and amounts of emissions allows for targeted interventions, such as upgrading tugboats to more efficient technologies or optimizing operational practices to reduce fuel consumption and emissions. Over time, these improvements contribute to a more sustainable maritime sector, aligning with global environmental goals and potentially leading to cost savings through more efficient operations.

Competitive Advantage Through Transparent Emissions Data

Having transparent and reliable emissions data provides a distinct competitive advantage in the maritime sector. As regulatory and consumer expectations shift towards greater environmental responsibility, companies that can demonstrate effective emissions’ management through accurate data not only meet these demands but also differentiate themselves in the market. Transparent emissions reporting allows companies to showcase their commitment to sustainability, enhancing their reputation and appeal to eco-conscious clients and partners. This transparency, coupled with competitive service pricing, positions these companies as leaders in sustainability, making them more attractive in tender processes and partnerships where environmental impact is increasingly a deciding factor.

The implementation of the CSRD is indicative of a broader trend toward stricter environmental regulations and the expectation of more detailed data transparency. This regulatory shift encourages companies and their suppliers to not only comply with existing mandates, but to anticipate and prepare for future, more stringent requirements. By proactively enhancing their data collection and reporting systems, companies can ensure they remain adaptable and resilient in a regulatory landscape that is likely to evolve with increasing focus on sustainability. This forward-thinking approach not only minimizes future compliance risks, but also positions companies to take advantage of emerging opportunities related to sustainability advancements and innovations.

Conclusion

It is important to remember that the CSRD seeks to enhance ESG reporting and improve transparency across companies. While there might be some questions in the short term, the main objective is to ensure that businesses give stakeholders complete and credible ESG information in the future. Therefore, it is necessary to stay updated of any changes to the reporting requirements, while attempting to adapt to the existing. Not only does the CSRD and ESRS enhance transparency and accountability but also propel maritime companies, including tugboat operators, toward integrating robust ESG practices into their core operations.

The enactment of the CSRD and the ESRS signifies a shift in the maritime sector, impacting large and small companies. As the industry moves toward heightened transparency and standardized reporting, tugboats, as integral components of the maritime value chain, must adapt to these changes, ensuring their operations are accounted for within the broader scope of indirect, Scope 3 emissions. This requirement not only fosters greater accountability but also opens avenues for tugboat operators to enhance their sustainability measures.

Get data on your emissions with LionRock

As the CSRD and ESRS reshape the landscape of sustainability reporting, it’s crucial for maritime companies, including tugboat operators, to stay ahead. At LionRock Maritime, we provide guidance and support to help you meet these new regulatory requirements. Our team is here to assist you in refining your sustainability reporting processes and improving your ESG practices. Contact us to learn more about how we can support your journey towards compliance and sustainability.

Frequently Asked Questions

What are the aims of the CSRD and ESRS?

When did the ESRS become effective, and what are its requirements?

Which companies are required to report under the CSRD and when?

What are the implications of the CSRD for maritime companies, specifically tugboat operators?

Related Topics

New Tugboat Software: A Fuel Consumption Monitoring Alternative | 2024 Photo by Steve Doig on Unsplash Revolutionizing Tugboat Fuel Efficiency:…

References

- Press corner

- The Commission adopts the European Sustainability Reporting Standards

- Delegated regulation – EU – 2023/2772 – EN – EUR-Lex

- Directive – 2022/2464 – EN – CSRD Directive – EUR-Lex

- How the global shipping industry may be impacted by the European Corporate Sustainability Reporting Directive (CSRD)

- CSRD and ESRS: the relationship explained

- CSRD: Decoding shipping’s ESG era ahead of EU’s landmark directive

- Unveiling CSRD – its ripple effect on transport and logistics

- ESRS Sector Standards – EFRAG

- Incorporated Maritime Policy Concept: Adopting ESRS Principles to Support Maritime Sector’s Sustainable Growth

- Directive (EU) 2022/2464 of the European Parliament and of the Council of 14 December 2022 amending Regulation (EU) No 537/2014, Directive 2004/109/EC, Directive 2006/43/EC and Directive 2013/34/EU, as regards corporate sustainability reporting

- European Financial Reporting Advisory Group. Draft European Sustainability Reporting Standards, a Cover Note for Public Consultations. April 2022.

- The ESRS per delegated act (published in the OJ on 22 December 2023).

- CSRD timeline: what you need to report and when

Related Posts

The Impact of CSRD and ESRS on Maritime Sustainability Reporting

The Impact of CSRD and ESRS on Maritime Sustainability Reporting Photo from Ronan Furuta The Impact Of CSRD And ESRS On Maritime …

The Role of AIS Tracking Systems in Enhancing Maritime Operations

The Role of AIS Tracking Systems in Enhancing Maritime Operations Photo by MICHAEL CHIARA – Unsplash AIS Marine Traffic – AIS Tracking …

Green Ports: Decarbonizing Ports through Data and make Ports more efficient Image by 12019 from Pixabay Green Ports: Decarbonizing Ports through Data …

Efficient Tugboat Fleet Management Analytics: Implementing a Tugboat Tracker System Photo by Elijah Mears on Unsplash Optimizing Tugboat Operations: The Power of …